Category: Blog

-

Snapchat, By Some Numbers

Snap Inc., maker of the Snapchat app and face-mounted camera glasses called Spectacles, filed its S-1 with the SEC this past week, the first major step toward going public. I thought it’d be interesting to compare Snap Inc. to Facebook, considering that Snap CEO Evan Spiegel’s IPO roadshow message is that his company is “The…

-

Great Tech Podcasts From Off The Beaten Path

If you’re involved in the tech industry and like to listen to podcasts, chances are you’ve already heard the standard-issue stuff that consistently ranks at the top of iTunes. Shows like Exponent (of which I am particularly fond), the a16z Podcast, Startup from Gimlet Media, and even NPR offerings like How I Built This and…

-

2016: My Year In Writing, And Goals For 2017

Since (finally) graduating from college in March and spending much of April on a couch recuperating, I spent the latter three quarters of 2016 doing a lot of writing, both for money (from Mattermark and other clients) and for pleasure (i.e. in my personal blog, in The Missive and my newsletter). A look back at 2016…

-

-

Of Apple & Courage

This past week, Apple announced a number of things at a special event in San Francisco. Among them was the latest iPhone model which, controversially, did away with the 3.5 mm headphone jack. Company claims that this omission was “courageous” were met with sneers and jeers from the peanut gallery and media cognoscenti alike.

-

How to Compare Venture Returns & The Curious Case of a16z

The Wall Street Journal published an article shining a light on Andreessen Horowitz, the vaunted VC firm that seemingly came out of nowhere in 2009 to become one of the most prestigious venture firms in Silicon Valley. The article indicates that a few of a16z’s funds are not performing as well as their age-matched peers.…

-

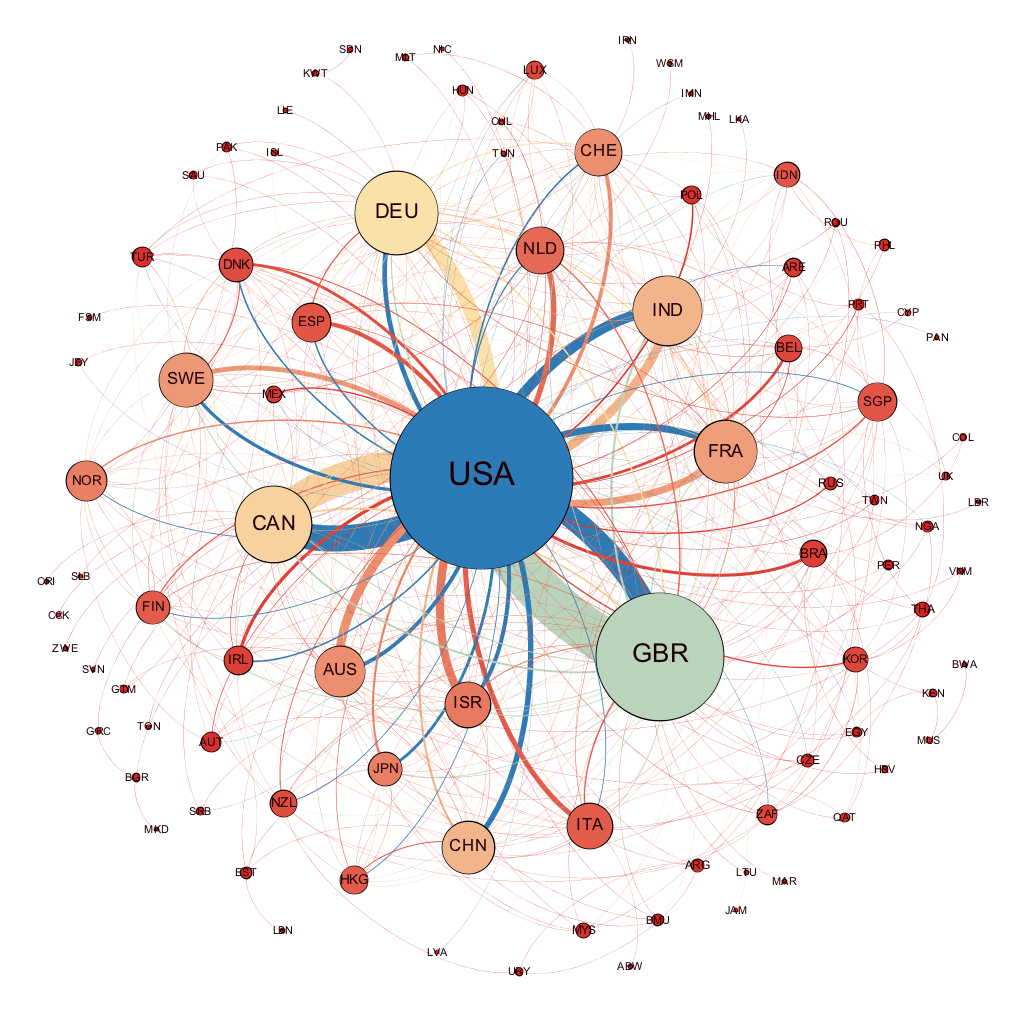

Dive Into Network Theory: Some Resources for The Curious

Earlier this week I published a piece for Mattermark’s blog that maps and visualizes the network of international mergers and acquisitions of startups and a few other private companies. To accomplished this, I used data from Mattermark recording 2,250 cross-border M&A deals made between January 1, 2015 and the end of August, 2015. The visualization…

-

Simple Security Best Practices for Bitcoin Users and Investors

One of the biggest stories to hit the Bitcoin space in months was the theft of 119,756 BTC (valued at ~$70 million USD) from Bitfinex this week. For those that aren’t familiar with the story, a great re-cap was published on CoinDesk within 24 hours of the break-in. (Obviously, if you’re reading this far into…

-

Virtual Reality, Already a Reality (for the Payments Industry)?

Note: This is the unedited version of an interview I gave to PCM, a payments industry trade journal produced by Payments & Cards Network. It is reprinted here with permission from the editor. In the interview I give a broad overview of the history of VR/AR and the unique challenges and opportunities presented by the…

-

The Risk Of Trusting In A Trustless System

Discussing the risks and challenges of trust in the Bitcoin ecosystem.